#117 Reality vs Rhetoric: CPF, Cash, Foreign Talent and Why Nuance Still Matters 现实与修辞:公积金、现金、外来人才,以及为什么“细节”仍然重要

#117 Reality vs Rhetoric: CPF, Cash, Foreign Talent and Why Nuance Still Matters 现实与修辞:公积金、现金、外来人才,以及为什么“细节”仍然重要

In an age where commentary spreads faster than context, public statements about national policies can shape perception almost instantly. Discussions about CPF, employment economics, and financial systems deserve more than simplified comparisons or selective framing. They require completeness, especially when they affect livelihoods, retirement security, and public trust.

This reflection is not about personalities. It is about accuracy, systems thinking, and responsible public discourse.

Employer Cost vs Employee Reality – Two Different Truths

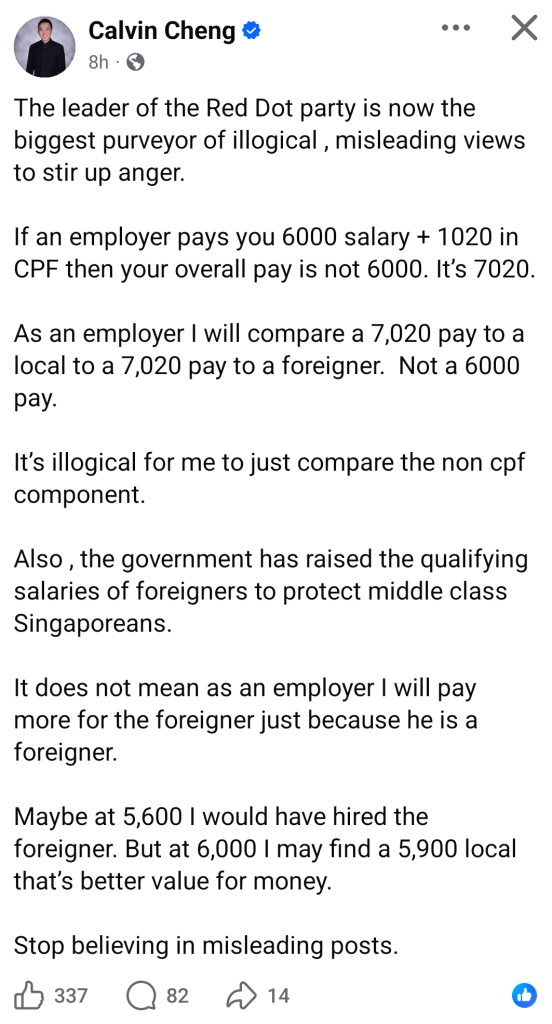

It is technically correct that if a Singaporean earns $6,000, the employer’s total cost is roughly $7,020 after CPF contributions.

But from the employee’s perspective:

- 20% CPF contribution = $1,200

- Actual take-home pay = $4,800

Both figures are factual. They simply measure different dimensions.

Highlighting only employer cost without showing employee disposable income creates a skewed impression of compensation. Meaningful discussions must present both perspectives simultaneously.

CPF Is Strong; But Not Fully Flexible

Singapore’s CPF system is widely recognised for its strengths:

- retirement adequacy discipline

- healthcare provisioning

- housing support

- prevention of old-age poverty

These achievements are real and significant.

However, acknowledging strengths should not prevent honest discussion of constraints Singaporeans experience:

- CPF funds are largely illiquid

- Withdrawal is restricted until eligibility age

- Usage is limited to approved purposes

- Practical usefulness often depends on housing affordability

For many citizens, CPF may represent substantial savings on paper but limited flexibility in real-time financial situations.

That does not make CPF flawed. It means CPF is a trade-off system by design.

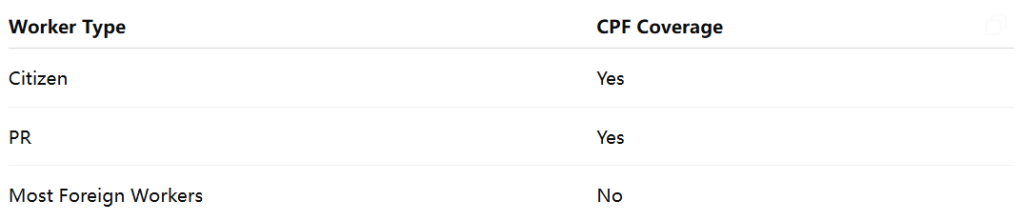

Foreign Worker Comparisons Require Precision

One widely repeated misconception is that foreigners benefit from CPF like locals.

In reality:

Most foreign workers do not receive CPF at all. Therefore real hiring comparisons often look like:

Local hire = known salary + employer CPF Foreign hire = salary only (plus levies where applicable)

Any blanket comparison that does not distinguish immigration status risks misleading readers about actual labour cost structures.

CPF Withdrawal Differences

Another nuance often omitted:

- PRs who leave Singapore permanently and renounce PR may withdraw CPF.

- Citizens generally cannot withdraw freely until retirement eligibility.

This difference exists because CPF is structured as a retirement system tied to long-term residency, not a liquid savings account.

Again, design choice, not oversight. But also, an important distinction.

Digital Payments vs Cash Resilience

Some commentators have argued that cash is obsolete in a digital economy, a view that previously triggered public backlash.

Yet infrastructure reality suggests otherwise.

If a nationwide payment network fails, or a cloud or data centre outage occurs:

- cards stop working

- transfers halt

- QR payments fail

Cash continues to function.

Cash is not outdated. It is financial redundancy infrastructure.

Digital = efficiency Cash = resilience

Strong systems retain both.

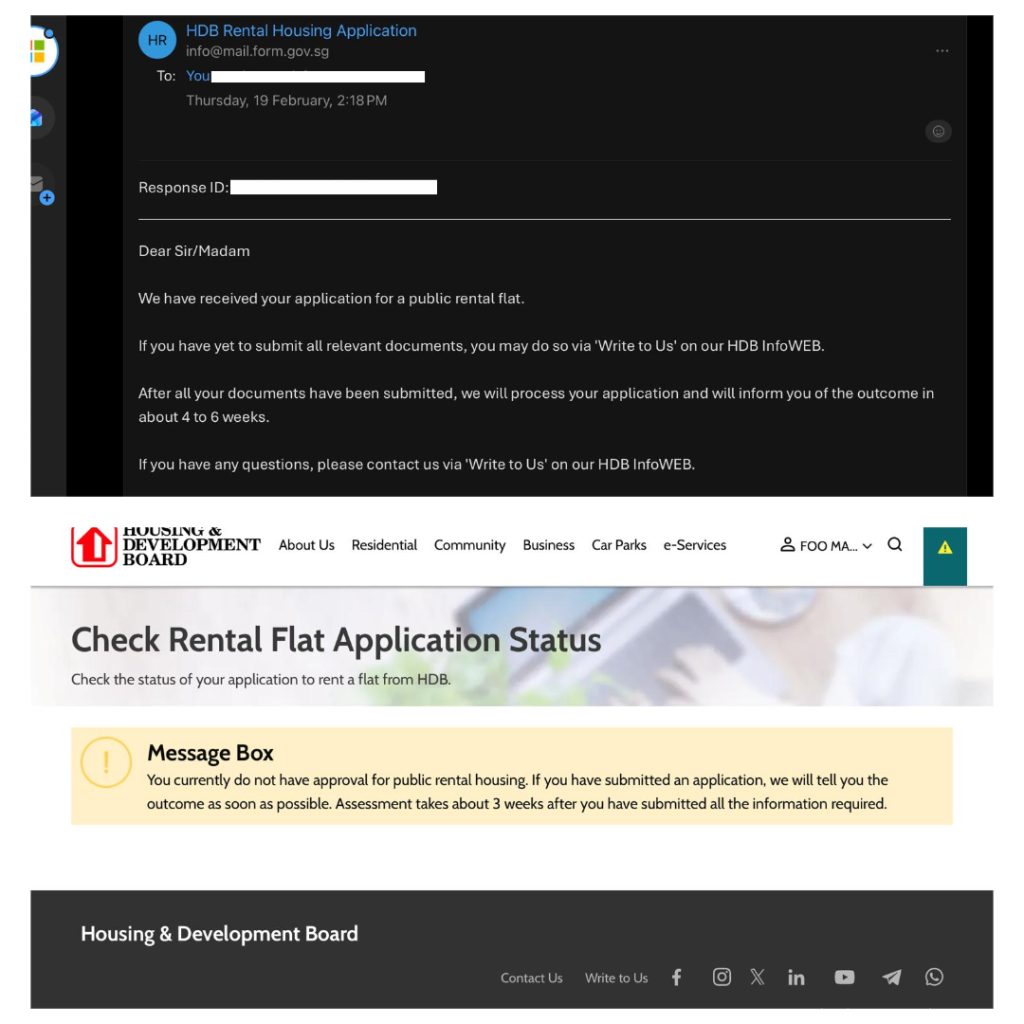

Administrative Systems Matter Too – Real Experiences from Readers

Beyond policy theory, real-world administrative experiences shape citizens’ daily realities.

Several readers recently shared feedback regarding housing assistance applications:

Reported observations

- Some applicants say HDB HFE-related processes no longer send acknowledgement emails.

- One public rental applicant received an email acknowledgement of submission but could not find a corresponding transaction record ID in the portal.

- The system displayed a Response ID, but not an application record ID usable for follow-up.

Why this matters:

Constituency-based Family Service Centres and social support teams often require formal reference IDs to track or support cases. When applicants cannot retrieve a recognised application ID, it can delay assistance for individuals who are already in vulnerable situations.

Even small administrative design gaps can have real human impact.

In policy design, user experience is not cosmetic; it is functional infrastructure.

Why Oversimplified Narratives Attract Pushback

Public figures who take rigid positions often draw responses from other experienced leaders and observers; not because disagreement is unusual, but because complex national systems rarely fit into binary conclusions.

Economic systems involve:

- multiple policy objectives

- trade-offs between flexibility and stability

- safeguards vs accessibility

- short-term pain vs long-term protection

Reducing such systems to single-variable explanations may be rhetorically powerful, but it risks weakening public understanding.

The Standard Public Discourse Deserves

Singapore’s long-standing policy strength has never come from slogans. It has come from careful calibration — balancing competing needs, evaluating trade-offs, and adjusting systems pragmatically.

Healthy national discussion should therefore:

- show full comparisons

- acknowledge trade-offs

- distinguish categories clearly

- prioritise clarity over virality

Final Reflection

CPF is not useless. Cash is not obsolete. Foreign manpower policy is not simple. Administrative systems are not trivial.

Reality is layered.

Strong opinions can spark attention. But only complete explanations build trust.

In a world full of commentary, credibility belongs not to the loudest voice, but to the most accurate one.

This article is also published on LinkedIn.

现实与修辞:公积金、现金、外来人才,以及为什么“细节”仍然重要

在这个信息传播速度远超事实核查的时代,公共政策的讨论往往被简化成几句引人注目的论述。关于公积金(CPF)、就业成本、外来人才以及现金是否“过时”的争论,正是一个典型例子。

这篇文章不是针对个人。 而是关于完整性、系统思维,以及负责任的公共讨论。

雇主成本 vs 员工现实 —— 两种不同的“真相”

如果一名新加坡公民月薪 6000新元,雇主的总成本约为 7020新元(包括雇主CPF供款)。

这是事实。

但从员工角度看:

- 员工需缴纳20% CPF = 1200新元

- 实际到手现金 = 4800新元

两个数字都正确。 但它们代表的是不同的维度。

如果只强调雇主的7020成本,而忽略员工的4800可支配收入,读者可能会误以为本地员工“实际拿得更多”。

公共讨论必须呈现完整的两面,而不是选择性地强调其中一面。

CPF制度是强项,但并非完全灵活

新加坡的CPF制度在国际上被广泛认可,其优势包括:

- 强制储蓄确保退休保障

- 医疗储备支持

- 促进住房拥有率

- 降低老年贫困风险

这些成就是客观存在的。

但与此同时,CPF对于普通工作中的新加坡人来说,也存在现实限制:

- 资金流动性有限

- 提款时间严格受限

- 使用范围被限定

- 实际效用高度依赖房价可负担性

当房价持续上涨、购房门槛提高时,CPF账户里的资金可能“账面充裕”,但在现实生活中却缺乏灵活性。

这并不是制度失败,而是制度设计的取舍。 但这种取舍必须被诚实地讨论。

外籍员工比较必须精确区分

一个常被忽略的事实:

大多数外籍员工并不享有CPF。

具体区分如下:

员工类别是否缴纳CPF新加坡公民是永久居民(PR)是大多数外籍员工(EP / S Pass / WP)否

因此,实际雇佣成本通常是:

- 本地员工 = 薪资 + 雇主CPF

- 非PR外籍员工 = 薪资(加上可能的外劳税)

如果不区分身份类别,就简单比较总成本,容易误导公众。

政策讨论需要精准,而不是笼统。

CPF提款差异

另一个重要区别:

- 永久居民若永久离境并放弃PR身份,可提取CPF。

- 公民一般需达到法定退休年龄才能提取。

这是制度设计逻辑 —— CPF是与长期居住绑定的退休制度,而不是随时可动用的储蓄账户。

这不是漏洞,而是政策选择。 但差异确实存在。

数字支付 vs 现金 —— 效率与韧性

有人曾公开表示,在数字时代,现金“没有意义”。这种观点曾引发强烈反弹。

我们可以思考一个现实问题:

如果全国支付网络瘫痪? 如果云系统或数据中心发生重大故障? 如果网络攻击导致电子支付暂停?

那时:

- 刷卡无法使用

- 转账系统停摆

- 二维码支付失效

现金仍然可以流通。

现金不是落后。 它是金融系统的“备用电源”。

数字支付带来效率。 现金提供韧性。

成熟的金融体系必须兼具两者。

行政系统体验:真实读者反馈

政策不仅是宏观框架,也体现在具体行政流程中。

有读者反馈关于HDB申请流程的体验:

- 有人表示,HFE申请似乎不再自动发送确认邮件。

- 一名申请公共租赁组屋的读者收到确认邮件,但在HDB门户系统中找不到可用于追踪的正式申请记录编号。

- 系统仅显示“Response ID”,但这并非家庭服务中心可用来支持个案的正式申请ID。

这带来什么影响?

基层家庭服务中心在协助申请人时,通常需要正式的交易或申请编号。若系统无法提供清晰记录,可能延误对弱势家庭的支持。

行政系统的细节,直接影响真实个体的生活。

为什么过度简化会引发批评

国家政策涉及多重变量:

- 长期稳定 vs 短期灵活

- 强制储蓄 vs 个人自由

- 数字效率 vs 系统韧性

- 外来人才吸引 vs 本地就业保障

将这些复杂系统简化成单一角度,虽然易于传播,但难以反映真实情况。

这也是为何某些过于刚性的立场,往往会引起其他权威人士的不同声音。

复杂社会,不适合简单答案。

我们需要什么样的公共讨论?

新加坡的成功从来不是建立在口号上,而是建立在:

- 实事求是

- 审慎权衡

- 系统设计

- 持续校准

健康的公共讨论应当:

- 呈现完整比较

- 承认制度优势与限制

- 精准区分类别

- 避免情绪化简化

最后的思考

CPF不是无用。 现金不是过时。 外籍人才政策不是单一变量。 行政系统体验也不是小问题。

现实是多层次的。

声音可以很大。 但真正建立信任的,是完整与准确。

在这个信息爆炸的时代,真正的公信力,来自细节。